Call (585) 256-0090

Call (585) 256-0090

The US Medicaid program provides health insurance to low-income individuals and families. However, because of the steep costs associated with long-term care, Medicaid planning is a growing trend for individuals with higher net worth as an alternative to spending down assets to qualify for benefits. Individuals can plan to meet eligibility requirements by legally restructuring their financial resources and maximizing their likelihood of being accepted into the Medicaid program.

Common Reasons to Engage in Medicaid Planning

There are many reasons to participate in Medicaid planning, including:

- Long-term Care Costs

Medicaid can help cover expensive long-term care costs. Medicaid planning can help prepare for the possibility that you or a loved one will need to qualify for benefits to offset costs for long-term care. - Protecting Assets

Medicaid has strict eligibility requirements, including limits on the number of assets you possess. Medicaid planning helps restructure these assets to ensure you qualify for health benefits when needed. - Estate Planning

Medicaid planning is often a key component of estate planning. By arranging your finances in a way that allows you to qualify for Medicaid, you ensure you have the resources you need to cover long-term health care costs while protecting assets for your heirs.

How Prevalent is the Need for Long-term Care?

According to the National Center for Health Statistics, approximately 65,600 regulated long-term care facilities in the US serve more than 8.3 million residents in various long-term care facilities, assisted living facilities, and nursing homes.

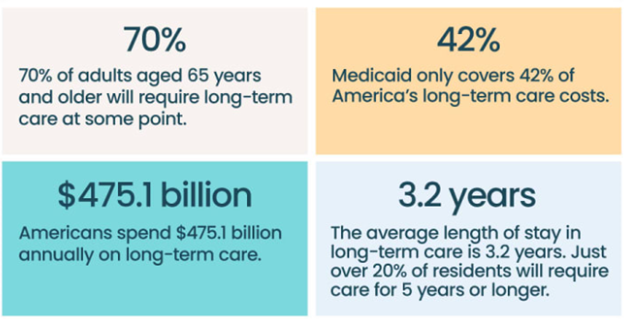

The percentage of individuals who will need long-term care is growing rapidly. According to the Administration on Aging (AoA), a division of the US Department of Health and Human Services (HHS), at least 70 percent of people aged 65 today will require some long-term care. This percentage continues to increase with age.

With an average stay of 3.2 years, Americans spend $475.1 billion annually to cover long-term care costs, and projections continue to climb. Medicaid benefits will cover approximately 42 percent of these costs making Medicaid planning crucial for financial solvency in retirement and legacy planning.

How to Begin Medicaid Planning

Taking the appropriate steps to legally and ethically protect assets while qualifying for Medicaid benefits is best handled by an elder law attorney in your state. Medicaid is a federal and state partnership program, and following your state’s rules and regulations is crucial to success. However, before engaging with an elder law attorney, you can gather some information to help them with your Medicaid planning strategy:

- Becoming familiar with your state laws and eligibility requirements regarding income and assets can streamline your consultation. Your attorney will answer all of your questions.

- Compiling a list of all assets, including savings, investments, property, insurance policies, and retirement accounts, can help your attorney determine which assets are exempt from Medicaid’s asset limits.

- Gathering information regarding all income sources will help your attorney figure out how much you can earn while still qualifying for benefits.

- Researching long-term care insurance policies helps decide whether you can afford to add it to your Medicaid strategy.

How an Elder Law Attorney can Help

After gathering the necessary financial information and any existing estate planning documents, it’s time to meet with your Medicaid planning or elder law attorney.

They will review your financial situation to determine what income and assets count toward Medicaid eligibility and identify any potential issues or challenges. Knowing your unique situation, your attorney can begin developing a custom strategy to comply with Medicaid rules and regulations.

Your Medicaid strategy must complement your estate planning documents and goals. An elder law attorney may amend existing will or trust documents to maximize Medicaid benefits and ensure a healthy spouse living at home has the financial resources they need.

An elder law attorney may recommend transferring assets into a Medicaid asset protection trust. The Medicaid lookback rules make it necessary to start this process at least five years before the need for care. When it's time to apply for benefits, your elder law attorney helps prepare and submit your Medicaid application.

You or a Loved One are Likely to Need Long-Term Care

Medicaid planning ensures you can afford the care you need. Because Medicaid eligibility is as important as it is complicated, an elder law attorney can ensure you qualify and avoid simple mistakes that result in a denial or delay of benefits. When planning for potential long-term care, the sooner you begin, the more options you have. Contact Rochester Elder Law to schedule a consult today.

more news you can use

Still have questions?

Tell us about your situation.

Centrally Located in Brighton

near Cobbs Hill:

1399 Monroe Avenue,

Rochester, NY 14618

Map & Directions

Weekly News & Updates

Subscribe now and get our FREE Guide, "The Top Eight Mistakes People Make with Medicaid Qualification"

{kind=link}

{kind=link}

{kind=link}

All Rights Reserved

Legal Disclaimer: The information on this website is for general purposes only and is not legal advice. Content may change without notice. Please consult an attorney for guidance on your specific situation. Contacting us does not establish an attorney-client relationship. Do not send confidential information until a formal attorney-client relationship is established. This site may contain attorney advertising. Prior results do not guarantee similar outcomes. By using this site, you agree to this disclaimer.